How to Plan for Retirement in New Zealand: Setting Financial Goals to Bridge the Gap

Securing your financial future and building wealth requires time, commitment, and a well-defined vision. With the growing retirement gap in New Zealand, early retirement planning is crucial for achieving long-term financial security.

As Benjamin Franklin once said, “If you fail to plan, you are planning to fail.”

Setting clear financial goals creates a roadmap that helps address potential retirement shortfalls while guiding you toward financial freedom.

This article explores how goal setting forms the foundation of a sound financial strategy, helping you identify potential retirement shortfalls and chart a course toward financial freedom.

Why Goal Setting is the First Step to Financial Success

The foundation of any good financial plan starts with setting clear goals. In fact, research published in the Harvard Business Review shows that those who set goals are 10 times more likely to be successful than those who don’t.

Goals provide direction, motivation, and a measurable path to follow. When building wealth, clearly defined goals help you focus on the bigger picture — such as buying a home, starting a business, or securing a comfortable retirement.

However, achieving financial goals can be challenging, not because we aren’t committed, but because life often throws unexpected curveballs.

This is why it’s important to build flexibility into your financial plan and remain adaptable as circumstances change. Even with life’s uncertainties, having clear goals can keep you anchored and ensure you stay on track toward long-term financial success.

Assessing Your Current Financial Position

Before you can plan for the future, you need to understand where you stand today. This involves clearly evaluating your savings, investments, debts, and income streams. Knowing your current net worth and cash flow allows you to evaluate your ability to save and invest toward retirement.

Many people avoid this step, but it’s vital for building a realistic plan. Conducting a personal financial audit gives you a snapshot of your current financial health.

Local Data and Statistics

To better understand your financial standing, it’s helpful to consider the bigger picture. Due to changing economic and demographic conditions, retirement planning is becoming increasingly critical in New Zealand.

For example, according to NCBI, the population of people aged 65 and older in New Zealand is projected to reach approximately 1.42 million in 2043, with further growth expected to be 2.06 million by 2068.

Furthermore, the average KiwiSaver balance for New Zealanders as of 2024 is approximately $31,823 (a 16.2% increase from $27,379 last year), which may not suffice for a comfortable retirement, suggesting a significant retirement savings gap.

Defining the Lifestyle You Want in Retirement

What do you want your retirement to look like? This is a highly personal decision that should guide your financial and retirement planning.

-

Do you plan to travel during retirement?

-

Would you like to buy a holiday home?

-

Are hobbies and leisure activities a key focus for your retirement?

-

Would you like to dedicate time to volunteer work or community projects?

-

Do you see yourself pursuing new personal ventures or experiences?

Your ideal retirement lifestyle will determine how much money you’ll need, shaping your savings goals and informing your investment strategy. It’s essential to think beyond basic living costs and consider lifestyle choices that will bring you fulfillment.

If your goals include frequent travel, early retirement, or supporting your children financially, these should guide how you structure your plan.

How Much Will You Need? Calculating Your Retirement Shortfall

Once you know the lifestyle you want, it’s time to calculate the gap between where you are now and where you need to be—often referred to as your retirement shortfall.

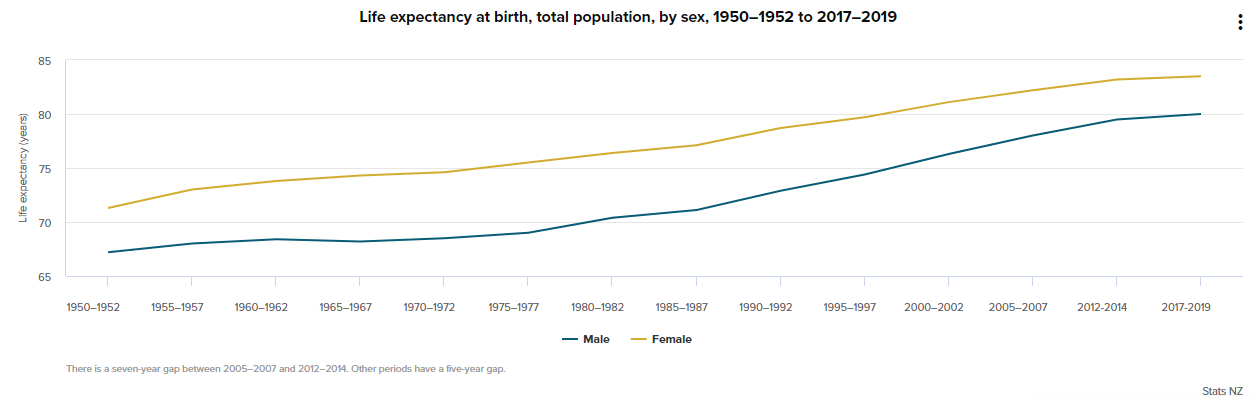

To effectively plan for this shortfall, it’s essential to consider your expected lifespan based on current trends. With advancements in healthcare and living standards, people live longer than ever. In New Zealand, statistical data shows that about 80% of men aged 65 are expected to live until at least 90, while women of the same age have a life expectancy of up to 94.

Image source: Stats NZ

Retirement dynamics are shifting as there's no mandatory retirement age, and NZ Superannuation is accessible from age 65, whether or not you keep working. Increasingly, many choose to work beyond 65, full-time or part-time, impacting retirement planning strategies.

Considering these factors, calculating your retirement shortfall involves estimating future expenses, adjusting for inflation, and subtracting expected incomes from sources like KiwiSaver and pensions. This reveals the financial gap you need to fill with additional savings.

Sample Calculation

Here’s a practical example of estimating retirement shortfall in New Zealand:

Step 1: Defining the Retirement Age and Duration

- Retirement Age: 65 years old

- Expected Retirement Duration: 20 years (until age 85)

Step 2: Estimating Annual Retirement Expenses

- Basic Living Expenses (food, utilities, etc.): $25,000 per year

- Healthcare and Insurance: $5,000 per year

- Leisure and Travel: $10,000 per year

- Total Annual Expenses: $40,000 per year

- Adjust for Inflation (2% per year over 20 years): $40,000 * (1.02^20) ≈ $59,460 per year by the time of retirement

Step 3: Assessing Expected Retirement Income

- KiwiSaver Fund (estimated balance at retirement): $300,000

- Assuming a withdrawal rate of 4% per year: $12,000 annually

- Government Pension (New Zealand Superannuation): Approx. $20,000 annually for a single person living alone

- Other Investments (real estate, dividends, etc.): $10,000 annually

- Total Expected Annual Retirement Income: $42,000 per year

Step 4: Calculating the Annual Shortfall

- Estimated Annual Expenses at Retirement: $59,460

- Total Expected Annual Income: $42,000

- Annual Shortfall: $59,460 - $42,000 = $17,460

Understanding your retirement shortfall is critical, as it highlights how much you need to accumulate through focused investment goals to sustain your desired lifestyle throughout retirement.

This calculation often serves as a wake-up call, prompting immediate action to strategically close the gap.

Developing a Financial Roadmap to Bridge the Gap

After identifying your retirement shortfall, the next step is developing a plan to bridge it. This is where it becomes important to create a financial roadmap—a clear and actionable strategy to achieve your goals.

This roadmap could include increasing your KiwiSaver contributions, setting aside more savings, or exploring other investment vehicles, such as Property or shares, to help grow your wealth.

For many, it might also involve seeking professional financial advice to ensure you're on the right track. In New Zealand, the sooner you start implementing a savings and investment strategy, the more time your money has to grow and compound.

Importantly, your financial roadmap must account for life's inevitable surprises, ensuring you can remain on track even when faced with the unexpected.

Additional Tips for Sourcing Retirement Funds:

As you refine your retirement planning strategy, consider these additional sources of funds beyond NZ Super, KiwiSaver, savings, and traditional investments:

- Reverse Mortgages: Use your home's equity to create an income stream without moving out, helping maintain financial stability during retirement.

- Iwi-based Savings Schemes: Explore community-based funds offering tailored retirement savings options for local needs.

- Debt-free Equity Release: Access the value tied up in your home without taking on extra debt, providing more financial flexibility.

- Downsizing Your Home: Selling your current home and moving to a smaller property can free up capital for your retirement needs.

- Take in a Boarder: Renting out a room to generate extra income can be a simple way to supplement your retirement funds.

- Rent Out Part of Your Home: This could refer to renting a separate part of the house, such as a basement or granny flat, for more privacy or even short-term rentals like Airbnb.

- Subdivide Your Property: If your property size allows, subdividing and selling part of it can provide a financial boost.

- Sell Your Home to Family or Whānau: Selling your home while retaining the right to live in it can give you access to funds while maintaining a secure living arrangement.

The Power of Good Habits: How Early Action Sets You Up for Success

Establishing good financial habits is essential for long-term wealth and security, especially in a high-cost city like Auckland. Setting clear goals and regularly reviewing them enables small adjustments that, over time, lead to significant progress. Remember, these small tweaks compound into lasting change.

Starting early is key. Compound interest in your savings and property investment allows modest contributions to grow into substantial wealth by the time you retire. Key habits, such as setting up automatic savings, conducting regular financial checkups, and continuously educating yourself, provide the consistency you need to reach your financial goals.

Take Note: The earlier you begin, the more flexibility you'll have to adjust and grow your wealth. With consistency and early action, the financial goals you set today can transform into the secure retirement you desire.

Conclusion: Plan Now for the Retirement You Want

Wealth-building and retirement planning don’t happen overnight. It requires time, thoughtful planning, and disciplined goal-setting.

Identifying your retirement shortfall early and creating a financial roadmap to bridge that gap allows you to confidently work toward your desired future while avoiding unpreparedness.

Even when life throws unexpected challenges your way, a clear plan will keep you focused on your long-term financial goals. The sooner you take action, the more time you allow your money to grow and compound, putting you in the best position for a secure and fulfilling retirement.

Ready to start your wealth-building journey? Book a free consultation with one of our experienced consultants today to discuss your goals and explore how we can help you achieve the retirement of your dreams.

Let’s work together to create a personalised financial plan that sets you on the path to achieving your retirement goals and dreams.